Featured

The U.S. Tax

Code:

A Giant

Spreadsheet

Monster

Wearing

a Tiny HatThe U.S. Tax Code:

A Giant Spreadsheet

Monster Wearing

a Tiny Hat

A playful deep-dive into the most illogical, arbitrary, and inconsistent rules in federal income tax law.

Here is the basic idea of an income tax:

Money comes in

- real costs of earning that money

= incomeThen the government says, "Cool, please give us some of that." This is not, by itself, insane.

The Internal Revenue Code starts with a normal-sounding rule: gross income means all income from whatever source derived, including wages, business income, gains from property, interest, rents, royalties, and dividends. Then Section 162 says businesses can deduct ordinary and necessary expenses. [LII section 61] [LII section 162]

Taxpayer: I made income.

Tax Code: Great. We tax income.

Taxpayer: I had costs to earn it.

Tax Code: Fine. We tax net income.That is the reasonable little village at the base of the mountain. Then you climb the mountain. At the top is a castle full of exceptions, phaseouts, special definitions, magic tunnels, cliff edges, and one rule that appears to have been written by a horse.

Meet the Tax Code Monster

Imagine Congress owns a zoo. But instead of animals, the zoo has tax rules.

Business deduction = Labrador

Capital gain preference = suspicious fox

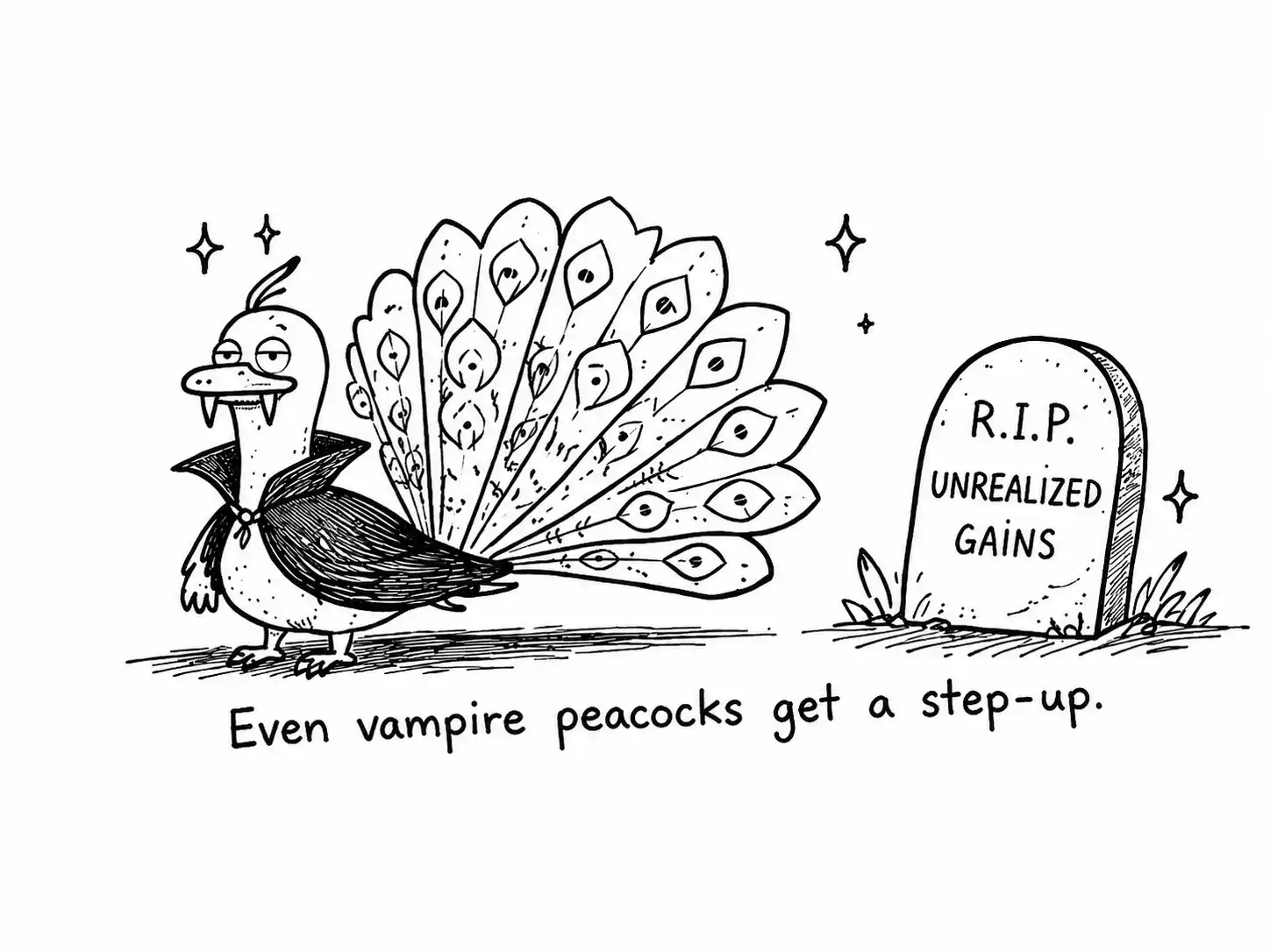

Step-up in basis = immortal vampire peacock

Section 280E = angry crocodile with an accounting degree

Section 199A = octopus made of worksheetsThe problem is not that tax law has exceptions. A tax system needs exceptions. It has to deal with families, businesses, investments, homes, losses, fraud, charities, foreign income, and people who try to describe their yacht as a consulting platform.

The problem is that many exceptions do not follow a principle. They follow politics, timing, ownership form, asset type, industry lobbying, or the ancient congressional method known as "eh, put it in the Code."

Step-up in basis at death

When you die, your assets get a glow-up.

All that appreciation? Poof - gone. The tax code rewards you for not needing the money anymore.

The tax rule: when someone dies owning appreciated property, the heir generally gets a basis equal to fair market value at death. Treasury regulations describe the general Section 1014 rule as giving inherited property a basis equal to its fair market value at the date of death, or alternate valuation date if elected. [eCFR section 1.1014-1]

Grandma buys stock for $100,000.

Grandma dies when it is worth $1,000,000.

Heir sells it for $1,000,000.

Income tax system: "What $900,000 gain?"This is called step-up in basis. From an income-tax logic perspective, it is the giant blinking sign that says labor income is taxed now, capital gain is taxed later, and capital gain held until death can disappear.

The weirdness is not just that death is important. Death is obviously important. The weirdness is that death can act like a magic eraser for income-tax purposes.

A worker cannot die and cause last year's wages to become untaxed. A consultant cannot say, "My invoice appreciated spiritually." A restaurant cannot hold its sandwich income until death and step up the basis of the sandwiches.

But an appreciated asset can sit there, quietly becoming more valuable, and if the owner wins the biological waiting game, a big chunk of economic income can vanish from the income-tax base.

The defenders have real points. Valuing assets at death can be hard. Closely held businesses can be illiquid. Farms are not checking accounts. The estate tax overlaps somewhat. But if the income tax is supposed to tax income, this rule is still the vampire peacock: beautiful to the taxpayer, hard to kill, and conceptually undead.

Section 280E

Run a legal cannabis business?

Great! Now pay tax on your income without getting normal business deductions. Good luck.

Normal tax law says a business deducts ordinary and necessary business expenses. Then Section 280E walks in wearing sunglasses and says: not you.

Section 280E denies deductions or credits for businesses trafficking in Schedule I or II controlled substances prohibited by federal or state law. The statutory text says no deduction or credit is allowed for amounts paid or incurred in carrying on that trade or business. [26 USC 280E]

Revenue - expenses = taxable income

Revenue - some inventory costs - nope - nope - nope = taxable income-ishThis is a tax-law identity crisis. If a business pays rent, wages, insurance, compliance costs, payroll, legal fees, and security costs, those are real costs. Pretending they do not exist does not make the business more profitable.

The cannabis example makes the rule even stranger. In April 2026, DOJ and DEA issued a final rule placing FDA-approved marijuana products and marijuana subject to a state medical marijuana license into Schedule III, effective April 28, 2026. The notice says state licensees will no longer be subject to Section 280E's deduction disallowance, while other marijuana remains Schedule I. [Federal Register final rule]

Are you marijuana?

Are you medical marijuana?

Are you state-licensed medical marijuana?

Are you FDA-approved marijuana?

Are you other marijuana?

Are you marijuana but wearing the wrong regulatory hat?That is not income-tax logic. That is controlled-substance classification doing accounting. The public-policy instinct is understandable, but the income tax is supposed to measure income. If Congress wants a penalty, it should impose a penalty.

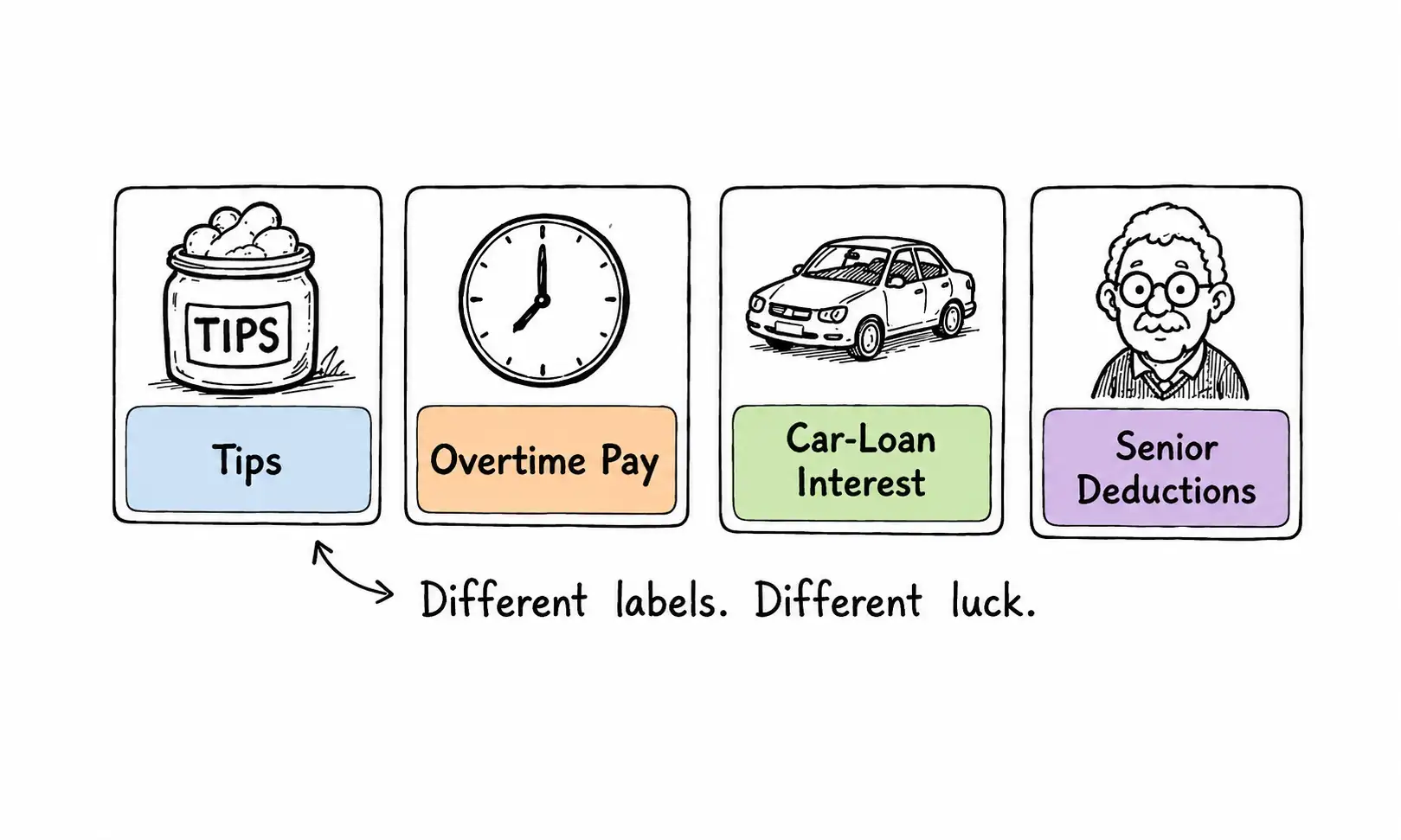

The label-based deductions

If Congress likes the label, you get the break.

If not, tough.

In 2025, Congress added temporary deductions for tips, overtime, car-loan interest, and seniors through the One Big Beautiful Bill Act, which IRS says was signed into law on July 4, 2025, as Public Law 119-21. [IRS OBBB provisions]

No tax on tips: up to $25,000 deduction for qualified tips in IRS-identified tipped occupations.

No tax on overtime: up to $12,500, or $25,000 joint, for qualified overtime premium pay.

No tax on car loan interest: up to $10,000 for interest on qualifying personal-use vehicle loans.

Senior deduction: $6,000 per eligible person age 65 or older, subject to income phaseouts.The tips rule is tied to occupations customarily and regularly receiving tips on or before December 31, 2024. The overtime deduction generally covers the premium portion of overtime pay, and the car-loan interest rule applies only to qualifying personal-use vehicle loans, with leases excluded. [IRS individuals and workers]

Worker A earns $50,000 in wages.

Worker B earns $40,000 in wages + $10,000 in tips.

Worker C earns $40,000 at Job 1 + $10,000 at Job 2.

A: regular income.

B: ah, special bucket!

C: regular income again.Economically, these people may be very similar. Tax Code-wise, the dollars get sorted by costume. Extra hours at one employer may be special; a second job may just be more income.

New qualifying U.S.-assembled vehicle loan interest: maybe deductible.

Used car loan interest: no.

Lease: no.

Bus pass: no.

Emergency car repair loan: no.

Walking to work in the rain: character building.This is the Tax Code playing dress-up. It is not asking, "How much income do you have?" or "How much ability to pay do you have?" It is asking, "What costume is your income wearing?"

The senior deduction has a similar cliff flavor: age 64 is normal; age 65 unlocks a special deduction universe. Seniors may need relief. The oddity is using a blunt age switch instead of targeting need, medical costs, retirement status, or actual ability to pay.

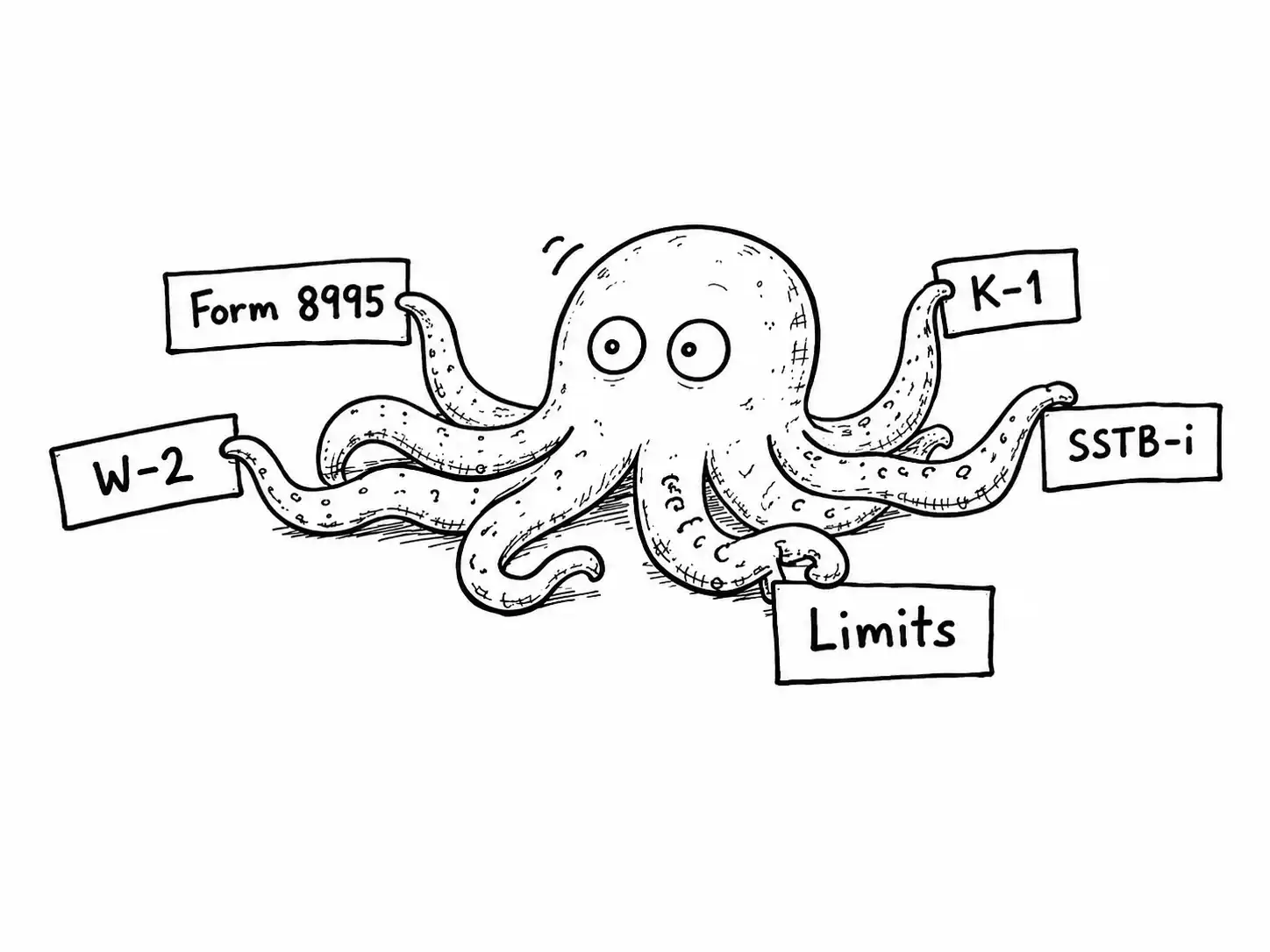

Section 199A

A deduction so complex it needed its own choose-your-own-adventure book.

And several worksheets.

Section 199A is the qualified business income deduction. IRS describes it as allowing eligible taxpayers to deduct up to 20 percent of qualified business income, plus certain REIT dividends and publicly traded partnership income. [IRS QBI deduction]

Are you a C corporation? No.

Are you a pass-through? Maybe.

Is it QBI? Maybe.

Are you in a specified service trade or business? Maybe.

How much W-2 wage does the business pay?

How much qualified property does it own?

What is your taxable income?

Are we phasing something in?

Are we phasing something out?The weirdness is not just complexity. Complexity can be justified when it prevents abuse. The deeper problem is horizontal inequity: people with similar economic income can receive different treatment depending on entity form, occupation, payroll structure, and capital intensity.

A W-2 employee earning $200,000 from skilled labor is in one tax universe. A pass-through owner earning $200,000 from a qualifying business may be in another. Doctors, lawyers, consultants, landlords, manufacturers, and software founders can all end up in different parts of the maze.

The law was partly a response to corporate rate cuts. If C corporations got lower tax rates, pass-through owners wanted parity. That is a real policy problem. But Section 199A solves it by building a haunted escape room.

Business income gets X treatment.

Labor income gets Y treatment.

Here is why.

Section 199A instead asks for W-2 wages, UBIA, SSTB status, taxable income, QBI, REIT dividends, PTP income, and phaseout ranges.Housing: the government's favorite child

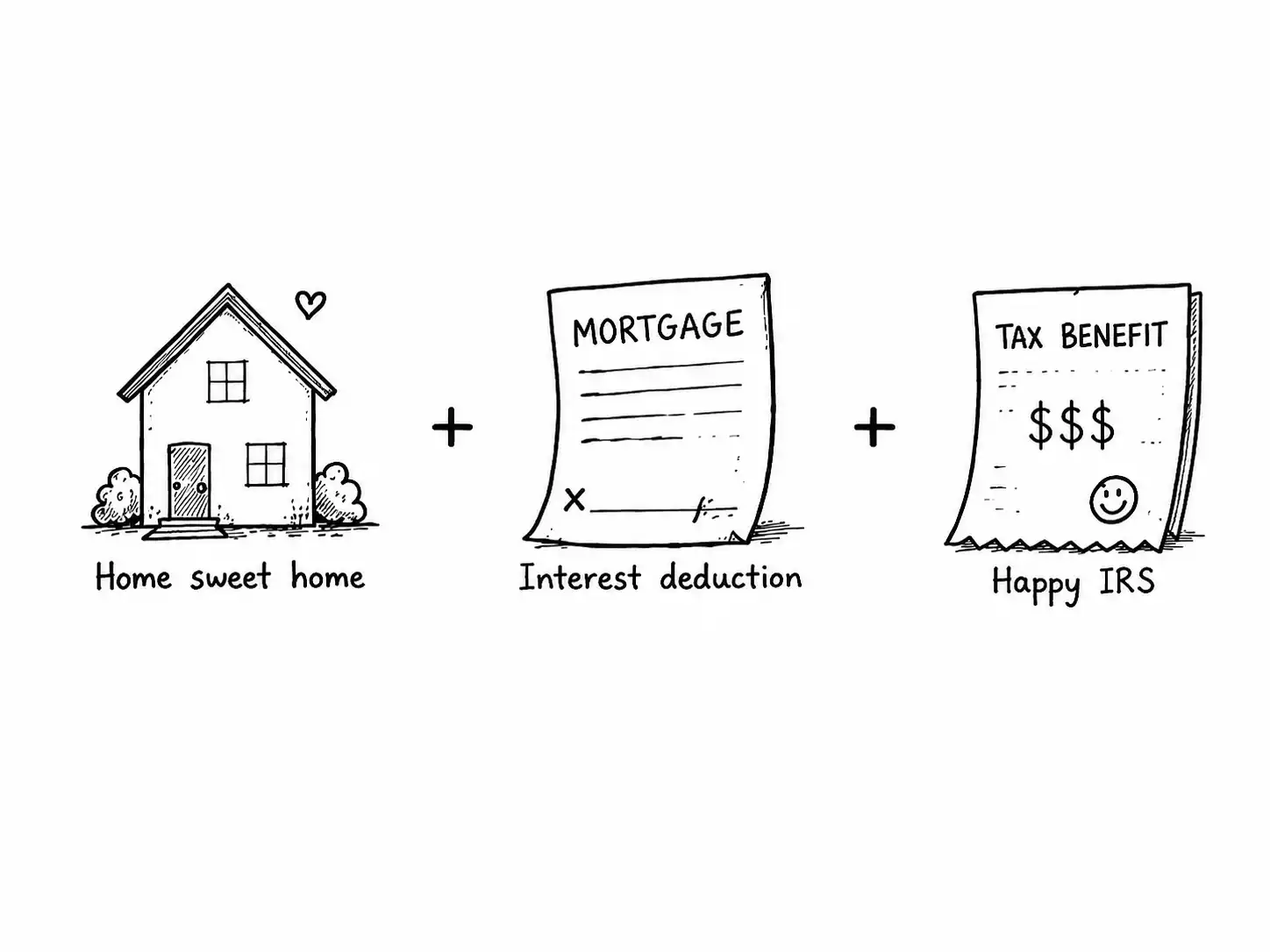

Buy a house, borrow a ton of money, and get a parade of tax perks.

Meanwhile, renters get... well, rent.

The Tax Code loves homes. Not shelter. Not housing affordability. Not renters. Homes. Specifically, owner-occupied homes with the right kind of debt, appreciation, tax payments, timing, and sometimes rental usage.

Home-sale gain exclusion

Mortgage interest deduction

State and local tax deduction

14-day rental income ruleThe home-sale exclusion

Section 121 excludes gain from sale of a principal residence if the taxpayer owned and used it as a principal residence for at least two years during the five-year period ending on the sale date. The exclusion is capped at $250,000, or $500,000 for many joint filers. [26 USC 121]

Stock gain: taxable.

Business asset gain: taxable.

Gold gain: taxable.

Home gain: maybe not.The home is not just shelter anymore. It is shelter wearing a tax invisibility cloak.

Mortgage interest

Section 163 generally disallows personal interest, but qualified residence interest is carved out. Current rules include the post-2017 $750,000 acquisition indebtedness limitation and disallowance of home-equity indebtedness interest under special post-2017 rules. [26 USC 163]

Credit card interest: personal, no.

Vacation loan interest: personal, no.

Mortgage interest: ah yes, civilization.

Certain car loan interest: temporarily yes, because reasons.SALT

Section 164 allows deductions for certain state, local, and foreign taxes, including state and local real property taxes, personal property taxes, and income taxes. SALT is partly about federalism, partly about housing, partly about high-tax states, partly about itemizing, and partly about Congress changing how much of it counts. [LII section 164]

The 14-day rental cliff

IRS says that if you use a dwelling unit as a residence and rent it for fewer than 15 days, you do not report the rental income and do not deduct rental expenses. [IRS Topic 415]

Rent your home for 14 days: income disappears.

Rent your home for 15 days: welcome to the rental rules.This is classic Tax Code cliff behavior. One more day and the floor changes. A 14-day cutoff is administratively convenient. Fine. But convenient is not the same as logical.

Oddity 6

Capital losses and wash sales: old asset rules meet new assets

The anti-abuse principle makes sense; the categories feel preserved in amber.

Capital gains are taxed when realized. Capital losses are limited. Section 1211 says corporate capital losses are allowed only to the extent of capital gains. For noncorporate taxpayers, capital losses are allowed against capital gains plus only a limited amount against ordinary income. [LII section 1211]

Taxpayer: I lost $80,000.

Tax Code: You may use $3,000 against ordinary income.

Taxpayer: That's not much.

Tax Code: Correct.The asymmetry is obvious: capital gain is taxable now, while capital loss is slowed down. There is a reason for this. Without limits, taxpayers could harvest losses while keeping gains unrealized.

Then we get to the wash-sale rule. Section 1091 disallows a loss on the sale of stock or securities if the taxpayer acquires substantially identical stock or securities during the 30-day window before or after the sale. [LII section 1091]

That rule makes sense for stocks. But digital assets complicate the old machinery. IRS says income from digital assets is taxable and gives examples including cryptocurrency, stablecoins, and NFTs. [IRS digital assets]

Stock: wash-sale rule.

Crypto: property, taxable, but not textually the same as stock or securities.

NFT: taxable property, but what even is substantially identical here?Oddity 7

Employer health insurance: compensation with a fake mustache

Cash pay is taxable. Employer health coverage generally gets a different planet.

If your employer pays you cash, it is income. If your employer pays for health coverage, Section 106 generally says gross income of the employee does not include employer-provided coverage under an accident or health plan. [26 USC 106]

$15,000 cash salary increase = taxable.

$15,000 employer health coverage = generally excluded.Same employer. Same employee. Same economic world. Different tax planet. This is one of the biggest form-over-substance choices in the entire tax system.

The exclusion is deeply embedded in American health care, so ripping it out suddenly would be chaos. But as tax logic, it is peculiar. Compensation is compensation unless it enters through the health-benefits door.

It also creates distributional weirdness. Exclusions are generally more valuable to people in higher marginal tax brackets. Workers without employer coverage, part-time workers, gig workers, and employees at firms with weak benefits get less help.

Oddity 8

Hobby-loss rules: the horse enters the chat

A necessary anti-abuse rule becomes a facts-and-circumstances obstacle course.

Section 183 limits deductions for activities not engaged in for profit. It creates a presumption of profit motive if gross income exceeds deductions in three of five years. But for activities consisting mainly of breeding, training, showing, or racing horses, the statute swaps in two of seven years. [LII section 183]

Normal activity: profitable 3 out of 5 years? Okay, maybe business.

Horse activity: profitable 2 out of 7 years? Different runway.The anti-abuse idea is good. Without hobby-loss rules, people would deduct losses from activities that are basically personal consumption: the yacht as consulting office, the vacation home as research facility, the horse as startup.

But Section 183 gets subjective fast. Profit motive depends on facts and circumstances. That means audits, disputes, records, testimony, vibes, and sometimes horses.

The horse rule may reflect the economics of breeding and racing. Those activities can take longer to become profitable. But in the arbitrary-tax-law zoo, a specific horse runway is still hard to ignore.

Oddity 9

Passive activity losses: the 500-hour trapdoor

A real anti-shelter wall became an hours-and-status obstacle course.

Section 469 limits passive activity losses and credits. It also has a special rental real estate rule: for certain rental real estate activities with active participation, up to $25,000 can escape the general passive-loss limitation, with the amount phased out as adjusted gross income exceeds $100,000. [LII section 469]

The regulations then bring in material participation tests, including a more-than-500-hours test and a more-than-100-hours-and-no-one-did-more test. [LII temporary regulation]

Did you participate for more than 500 hours?

Did you participate for more than 100 hours?

Did someone else participate more?

Is this rental real estate?

Are you a real estate professional?

Did you keep a contemporaneous log or just wave your hands?The problem being solved was real. Tax shelters used to let high-income taxpayers buy losses and use them to shelter unrelated income. The passive-loss rules are a defensive wall, but defensive walls can become obstacle courses.

499 hours: passive.

501 hours: nonpassive.Oddity 10

Section 68: the hidden rate rule hiding inside deductions

Instead of saying the rate is higher, the Code sends taxpayers through deduction math.

Section 68 reduces itemized deductions by 2/37 of the lesser of itemized deductions or the amount by which taxable income exceeds the threshold where the 37 percent bracket begins. [LII section 68]

Congress: We want high-income taxpayers to get slightly less value from deductions.

Normal way: Change rates or cap deductions directly.

Tax Code way: Create a fraction named 2/37.A transparent system would say the top rate is X or the deduction is capped at Y. Section 68 says to calculate deductions, apply other limits, reduce them by a fraction tied to the top bracket, and pretend this is not rate policy.

Oddity 11

Municipal bond interest: income, unless the borrower is government-shaped

Interest is income, except when state and local borrowing gets a federal subsidy costume.

Interest is normally income. Section 61 includes interest in gross income. But Section 103 says gross income does not include interest on state or local bonds, except as provided in the statute. [LII section 61] [LII section 103]

Corporation borrows money and pays you interest: taxable.

State or local government borrows money and pays you interest: tax-exempt.The economic thing is the same: you lent money and got interest. The policy reason is not mysterious. Tax-exempt municipal bonds subsidize state and local borrowing, which can support public infrastructure.

Federal government forgoes tax revenue

-> investors receive tax-exempt interest

-> investors accept lower yields

-> state/local issuers borrow more cheaply

-> some benefit reaches public projectsOddity 12

Foreign earned income exclusion: the 330-day border dance

Cross-border relief becomes a midnight-counting travel puzzle.

The foreign earned income exclusion lets qualifying U.S. citizens or residents working abroad exclude a certain amount of foreign earned income. IRS says the 2026 maximum exclusion is $132,900 per person. [IRS FEIE amount]

One way to qualify is the physical presence test: IRS says you meet it if physically present in a foreign country or countries for 330 full days during a 12-month period. A full day means 24 consecutive hours from midnight to midnight. [IRS physical presence test]

330 days abroad: exclusion possible.

329 days abroad: tax problem appears.This rule has a purpose. Americans abroad can face double taxation or compete in labor markets where local tax systems differ. But the day-count method is crude. Two people with the same income and same economic ability to pay can receive different federal treatment because one spent enough midnights abroad and the other did not.

Oddity 13

Energy credits: the subsidy pinata

Industrial policy is stapled to income tax returns, one expiration date at a time.

Energy tax credits are not really income-tax rules. They are industrial policy delivered through tax returns.

The 2025 law changed many clean-energy provisions. IRS guidance says the Act accelerated the end of several clean vehicle credits so that new clean vehicle, used clean vehicle, and qualified commercial clean vehicle credits are not allowed for vehicles acquired after September 30, 2025. It also says the energy efficient home improvement credit and residential clean energy credit are not allowed after December 31, 2025, under the relevant rules. [IRS OBBB provisions]

Meanwhile, the Section 45Z clean fuel production credit was extended for fuel sold before January 1, 2030, with detailed rules about feedstocks, emissions rates, foreign entities, sustainable aviation fuel, and other categories. [IRS OBBB provisions]

Bought on September 30: maybe credit.

Bought on October 1: nope.

This feedstock: yes.

That feedstock: no.

This vehicle: yes.

That vehicle: no.Tax credits can be legitimate. Sometimes the government wants to subsidize behavior. The issue is that the income tax becomes a constantly changing subsidy vending machine.

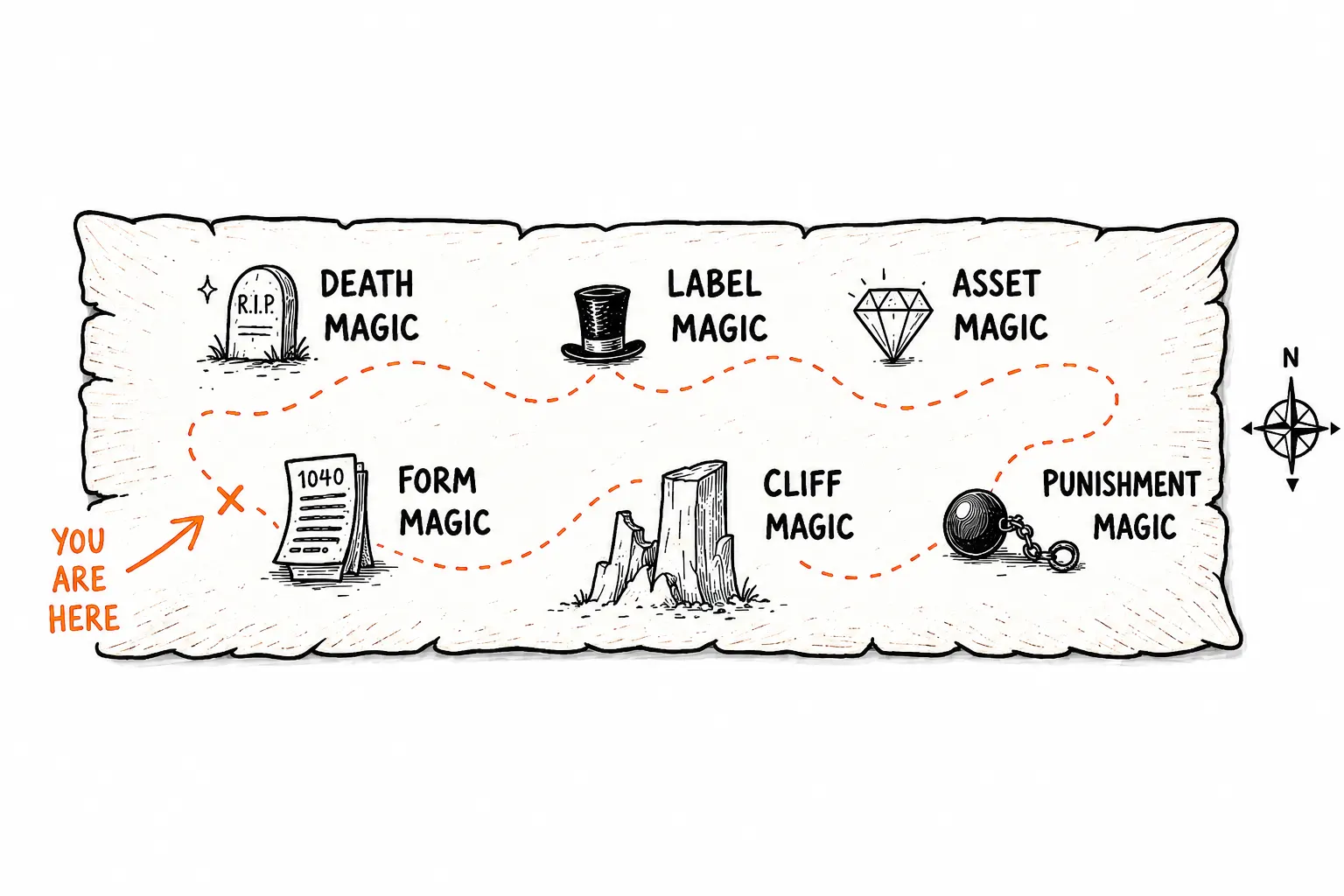

The Tax Code's Weirdness Map

Wander at your own risk.

If we map these rules by type of weirdness, the pattern is obvious.

1. Death magic -> step-up in basis

2. Label magic -> tips, overtime, car-loan interest, employer health benefits

3. Asset magic -> homes, municipal bonds, capital gains, energy credits

4. Form magic -> Section 199A, pass-throughs, entity choice

5. Cliff magic -> 14 rental days, 330 foreign days, 500 participation hours, age 65

6. Punishment magic -> Section 280E

7. Anti-abuse magic that got weird -> hobby losses, passive losses, wash salesEconomic substance: similar.

Tax result: wildly different.

Reason: label / timing / status / form / category.That is the heart of the problem. The Code keeps changing the tax result based on the wrapper the income arrived in.

The grand theory

A clean income tax would mostly ask three questions: how much economic income did you receive, what costs did you incur to earn it, and what is your ability to pay?

Did you inherit the asset?

Was the income called a tip?

Was it overtime?

Was the business a pass-through?

Was the worker an employee?

Did the employer buy health insurance?

Was the bond issued by a city?

Was the house rented for 14 days or 15?

Were you abroad for 330 full days?

Was the marijuana in the right legal bucket?

Did the horse lose money with sufficient dignity?That is how a tax system becomes a tax civilization. It has neighborhoods: Wage Town, Capital Gains Heights, Pass-Through Swamp, Real Estate Island, Municipal Bond Lagoon, Cannabis Deduction Desert, Foreign Earned Income Time Zone, and Horse Profit-Motive Ranch.

Some neighborhoods have low taxes. Some have high taxes. Some have gates. Some have invisible trapdoors. Some have a sign that says "Welcome, homeowners!" and another sign that says "Renters, please enjoy the standard deduction."

Final ranking

My totally subjective, probably inaccurate, but deeply felt ranking.

1. Step-up in basis at death

The champion. Income can disappear because the owner died holding the asset. If the income tax has a soul, Section 1014 is where it goes to argue with itself.

2. Section 280E

A net-income tax that denies real business deductions because of drug scheduling. Understandable as punishment, incoherent as income measurement.

3. Tips, overtime, car-loan interest, and senior deductions

The labels-are-policy zone. Similar income gets different treatment because Congress liked the words on the paycheck.

4. Section 199A

The pass-through octopus. Similar work can produce different tax results depending on entity form, occupation, wages, assets, and thresholds.

5. Housing preferences

Homeownership gets multiple overlapping favors. The 14-day rental rule is the tiny absurd cherry on top.

6. Capital loss and wash-sale rules

Good anti-abuse instincts, stale categories, and a $3,000 loss limit that feels like it was preserved in amber.

7. Employer health exclusion

Compensation is taxable, unless it is health coverage. Then it becomes invisible compensation.

8. Hobby-loss rules

Necessary anti-abuse law, but with a horse-shaped statutory detour.

9. Passive activity loss rules

Important anti-shelter rules that turned into an hours-and-status maze.

10. Section 68

A hidden rate adjustment disguised as an itemized deduction limitation.

11. Municipal bond interest

Interest is income, unless the borrower is a state or local government.

12. Foreign earned income exclusion

Reasonable cross-border relief with arbitrary day-count cliffs.

13. Energy credits

Industrial policy stapled to the income tax.

The punchline

The U.S. federal income tax is not one thing. It is two things.

The first is a serious system trying to tax income. The second is a giant political scrapbook where Congress keeps taping in exceptions.

Help homeowners.

Help seniors.

Punish drug traffickers.

Help pass-through businesses.

Subsidize state borrowing.

Help tipped workers.

Help clean fuel.

Help car buyers.

Protect against tax shelters.

Avoid taxing inherited appreciation.Each exception has a story. But together, they create a tax system where the biggest question is often not how much did you make. It is what kind of thing did the tax law decide you were doing?

That is why the Code feels arbitrary. Not because every strange rule is indefensible in isolation. Many have plausible explanations. The problem is that the explanations point in different directions.

The income tax wants to be a measuring device. Congress keeps using it as a remote control.

Primary sources and official guidance

Capital losses and digital assets

IRC sections 1211, 1091 and IRS digital assets